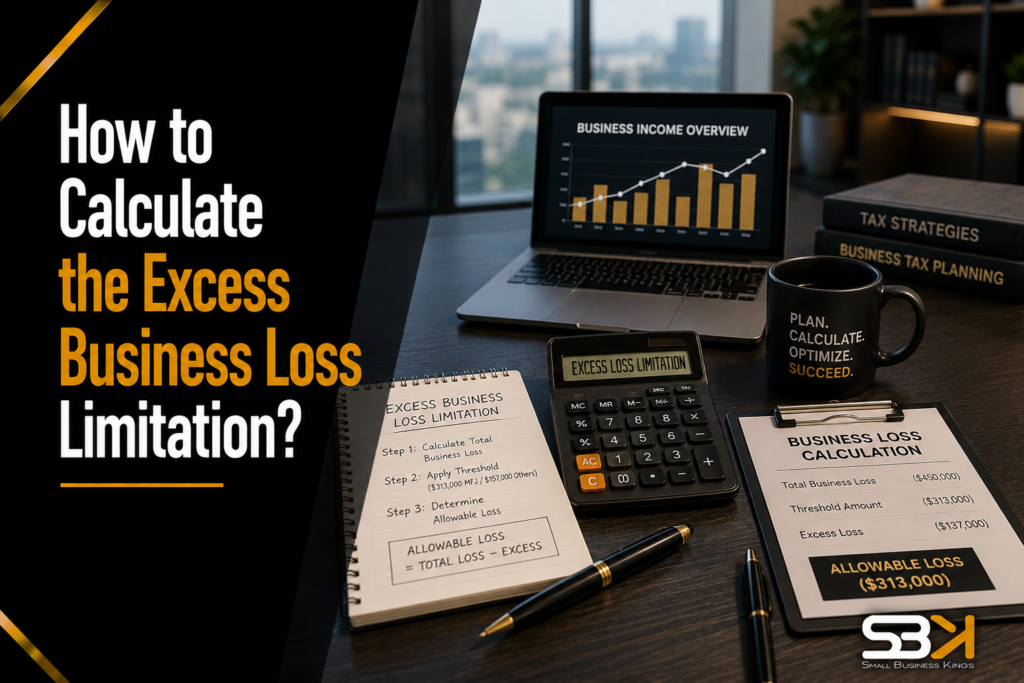

Once you know which losses have cleared the prior limitations, calculate your total trade or business gross income and gains, and separately your total trade or business deductions, across all your business activities for the year.

A “trade or business” for this purpose can include Schedule C (sole proprietorship) and Schedule F (farming) activities, as well as business activities reported on Schedule E through pass-through entities like partnerships and S corporations. Business gains and losses reported on Form 4797 (sales of business property) are also included in this calculation.

Specifically excluded from this calculation:

⚠ Slow site = lost salesLaunch on Solid GroundFast, secure VPS hosting for new businesses.Save 30%Get Started →

⚠ Slow site = lost salesLaunch on Solid GroundFast, secure VPS hosting for new businesses.Save 30%Get Started →- Wages, income, or deductions related to performing services as a W-2 employee. This is a meaningful distinction — your salary and any related deductions don’t factor into the business income/loss side of this calculation at all, even though the loss you’re trying to deduct might be offsetting that same salary.

- The Section 199A Qualified Business Income (QBI) deduction. This deduction is applied separately and isn’t part of the EBL computation itself.

- Certain capital gains and losses, which have their own specific inclusion rules — capital gain from the sale of business property is generally included, but the treatment of capital losses and gains from other capital asset trades follows separate, narrower rules. Confirm the specific treatment of any capital transactions with a tax professional, since misclassifying these is a common source of calculation errors.

Does the EBL limitation apply if my business itself was profitable this year?

No — the EBL limitation only comes into play when your total business deductions exceed your total business income and gains for the year, creating a net loss. If your business activities are net profitable, there’s no excess loss to test against the threshold.

What happens to the disallowed portion of my loss?

It’s treated as a Net Operating Loss (NOL) and carried forward to future tax years, where it can offset up to 80% of your taxable income in any given year until it’s fully used. This effectively defers the tax benefit rather than eliminating it.

Does my W-2 salary count as business income for this calculation?

No — W-2 wages and related deductions are explicitly excluded from the business income and deduction totals used in the EBL calculation, even though W-2 income is exactly the kind of non-business income that business losses would otherwise be limited from offsetting.

How do I know if my rental real estate income counts as business or non-business income?

It depends on whether you meet the IRS’s specific criteria to qualify as a real estate professional, which involves material participation and hours-based tests. If you don’t meet these criteria, rental income is generally treated as passive, non-business income; confirm your specific situation with a tax professional, since this determination is fact-specific.

Does the EBL threshold change every year?

Yes, it’s adjusted annually for inflation, but the adjustment isn’t guaranteed to increase — the threshold can decrease year to year depending on the inflation formula and any legislative changes. Always check the current year’s official IRS figures rather than relying on a prior year’s threshold.

Is the Excess Business Loss limitation permanent law?

As currently structured, it applies through the 2028 tax year, though it has been extended or modified in prior legislation and its future beyond 2028 is uncertain. Confirm the current status of this provision with a tax professional or the IRS’s current guidance before relying on it for multi-year planning.