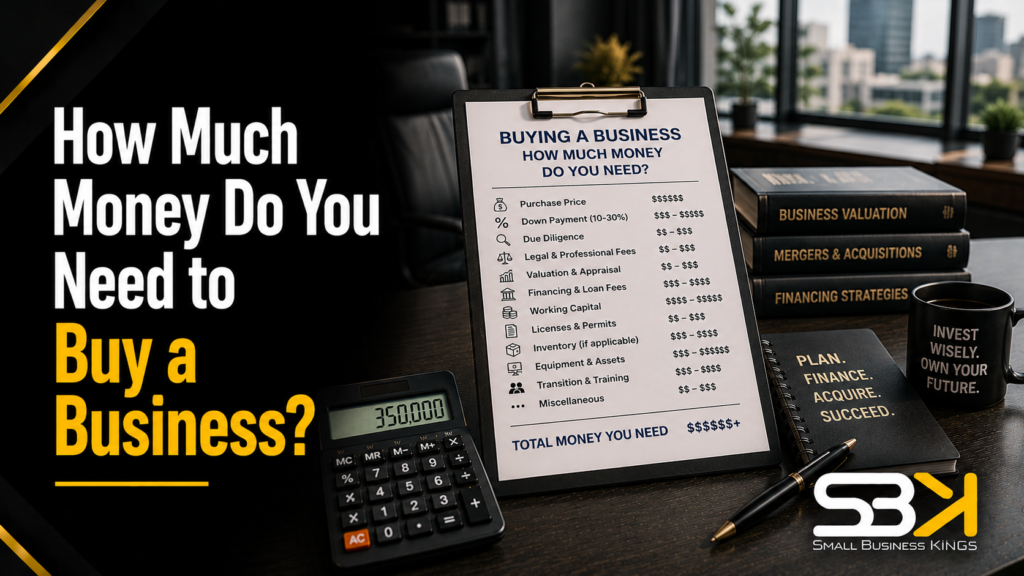

The purchase price is the headline number, but your down payment — the cash you personally contribute at closing — is what actually determines whether a deal is within reach. This depends heavily on how you finance the acquisition.

- SBA 7(a) loans: The SBA sets a minimum required equity injection for acquisition loans, and many lenders ask for more depending on the buyer’s experience, credit, and the business’s risk profile. Requirements can shift, so confirm current terms directly with the SBA or a participating lender [Source: U.S. Small Business Administration, SBA 7(a) Loan Program].

- Conventional bank loans: Generally require a higher down payment than SBA loans, along with stricter collateral and credit requirements, since there’s no government guarantee reducing the lender’s risk.

- Seller financing: The seller finances a portion of the price directly and gets repaid over time with interest. This can meaningfully reduce the cash you need upfront, but sellers still typically want a real down payment as proof of buyer commitment — seller financing rarely covers the entire deal.

- ROBS (Rollovers as Business Startups): Lets buyers use retirement funds, such as a 401(k), to fund part of an acquisition without triggering early-withdrawal penalties, through a specific IRS-compliant structure. This isn’t a simple do-it-yourself move — it requires proper plan setup and ongoing compliance to avoid tax consequences [Source: Internal Revenue Service, Rollovers as Business Startups Compliance Project].

- HELOC (Home Equity Line of Credit): Some buyers open a HELOC on their home before closing — not to use as the SBA equity injection itself, but as a standby reserve for working capital or unexpected costs after the sale.

The Cash Buyers Consistently Underestimate

The down payment gets all the attention, but three other cash categories matter just as much — and skipping them is the most common way buyers end up short on cash a few months into ownership.

Closing and Due Diligence Costs

Before you own anything, you’ll pay for the work of verifying the business is what the seller says it is: an accountant to review financials, an attorney to draft or review the purchase agreement, and possibly a valuation specialist. Lender fees and other closing costs stack on top of that. These fees vary significantly by deal size, complexity, and location — get direct quotes from your own advisors rather than budgeting off a number you saw in a blog post.

Working Capital

Working capital is the cash needed to keep the business running day-to-day right after you take over — payroll, inventory, rent — before revenue under your ownership fully replaces what the outgoing owner was generating. It’s typically calculated as current assets (cash, receivables, inventory) minus current liabilities (payables, short-term debt). This is frequently negotiated directly into the purchase agreement or letter of intent, and it’s one of the most commonly overlooked line items by first-time buyers.

A Post-Closing Reserve

Even a clean transition rarely goes perfectly. A key employee may leave once they hear about new ownership. A major customer may want to “wait and see” before recommitting. Equipment that was “recently serviced” may need attention sooner than promised. Buyers who go into closing with zero cushion beyond the purchase price are the ones most likely to panic in month two or three — not because the business is bad, but because they never budgeted for the ordinary friction of a transition.

How much cash do I actually need to buy a small business?

For a typical Main Street business financed with an SBA loan, expect a down payment plus separate cash for due diligence, closing costs, and working capital — the total is usually meaningfully higher than the down payment figure alone. The exact amount depends on the business’s price, your lender, and how working capital is negotiated in the deal.

Can you buy a business with no money down?

It’s uncommon and risky for a traditional acquisition, though combining seller financing with other structures can reduce the cash you need upfront. Most lenders and sellers want to see a real equity contribution from the buyer as evidence of commitment and reduced risk.

What’s the difference between a down payment and total closing cash?

The down payment is your equity contribution toward the purchase price itself, while total closing cash also includes due diligence and legal fees, working capital, and any post-closing reserve you set aside. Buyers who budget only for the down payment are often surprised by these additional costs at closing.

Is working capital included in the purchase price?

Not automatically — it’s frequently negotiated separately in the letter of intent or purchase agreement and can significantly affect the total cash a buyer needs at closing. Clarify working capital terms early in negotiations rather than assuming it’s baked into the headline price.

Can I use a HELOC as my SBA down payment?

Generally, HELOC funds are not treated the same as the buyer’s own equity injection for SBA loan purposes, so it’s typically used as a standby reserve rather than the down payment itself. Confirm current rules with your SBA lender, since loan program requirements can change.

What’s the difference between SDE and EBITDA when valuing a business?

SDE adds back the owner’s salary and personal expenses and is used mainly for smaller, owner-operated businesses. EBITDA doesn’t add back owner compensation and is typically used for larger businesses run by a management team rather than a hands-on owner.